Artificial intelligence remains one of the most powerful technological shifts of this decade. Adoption is accelerating, productivity gains are real, and nearly every major technology company now positions itself as “AI-first.”

And yet, markets are pulling back.

Across software, data, and AI-exposed sectors, share prices have declined sharply. For many investors, this feels counterintuitive: how can AI be booming while AI stocks are falling?

The answer is uncomfortable — but rational. What we are witnessing is not an AI collapse, but a market correction driven by fundamentals, timing, and expectations finally colliding.

This article breaks down what is actually happening beneath the surface, which AI subsectors are vulnerable, which are holding up, and what this shift means for investors and AI decision-makers alike.

Key Takeaway

The recent sell-off in AI and software stocks is not a rejection of artificial intelligence — it is a correction of expectations.

Markets are shifting from AI narratives to fundamentals, rewarding cash flow, pricing power, and execution while repricing companies built primarily on future promises.

For investors and decision-makers, the message is clear: AI remains a long-term driver, but returns will be increasingly selective.

The paradox of the AI boom

Over the past two years, AI was largely traded as a narrative.

Companies with even limited AI exposure benefited from valuation expansion based on future potential rather than present earnings. Multiples rose faster than revenues, and expectations moved far ahead of execution.

That works — until it doesn’t.

As macro conditions tighten and earnings scrutiny increases, markets shift their focus from what could happen to what is happening now. AI as a technology remains strong, but AI as a blanket investment theme is being re-priced.

This distinction matters.

What the market is actually doing

The recent sell-off is not isolated. It spans multiple segments of the technology stack, particularly:

- software-as-a-service platforms

- data and analytics providers

- AI platforms without clear profitability

- high-valuation companies with weak free cash flow

What stands out is selectivity. Companies with strong balance sheets, pricing power, and visible cash flows are holding up significantly better than those built primarily on future promises.

The market is not abandoning AI. It is discriminating.

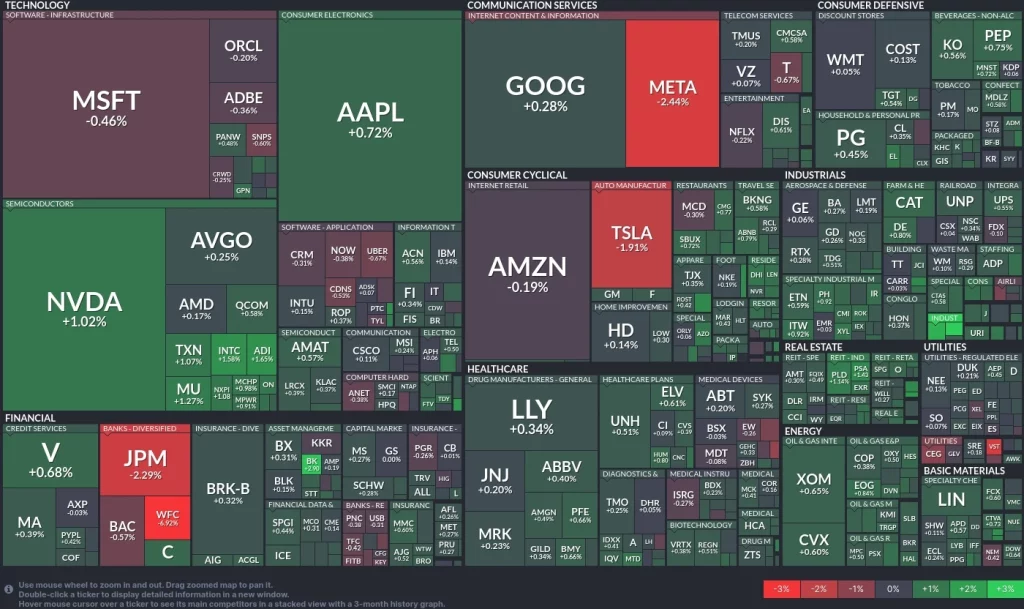

Market performance heatmap showing selective pressure across the tech sector.

The visualization highlights a broad pullback across software and AI-exposed segments, while companies with strong cash flows and pricing power remain relatively resilient.

Rather than a uniform sell-off, the market is differentiating sharply between:

- AI narratives without near-term profitability

- Capital-intensive software models under margin pressure

- Large, cash-generative technology leaders with structural demand

This pattern reinforces a key theme of the current correction: the market is not rejecting AI — it is repricing expectations and timelines.

AI enthusiasm versus fundamentals

At the core of the correction lies a timing mismatch.

AI investments typically share three characteristics:

- High upfront costs

Compute, infrastructure, talent, and model development require substantial capital. - Delayed revenue realization

Customers experiment cautiously. Scaling happens slowly, and ROI must be demonstrated. - Short-term margin pressure

AI often increases operating costs before efficiency gains materialize.

Many valuations priced in profitability several years ahead. As interest rates remain elevated and risk tolerance declines, markets are questioning how much uncertainty they are willing to underwrite.

The correction reflects skepticism about timelines — not doubt about AI itself.

Why software and data stocks are hit hardest

Software companies appear, on paper, to be ideal AI beneficiaries. They control distribution, own customer relationships, and sit on valuable data.

In practice, AI integration is costly and disruptive.

It often leads to:

- higher cloud and compute expenses

- product redesign cycles

- longer enterprise sales processes

- pressure on existing subscription economics

AI improves product capability, but frequently weakens margins in the short term. In a market environment that prioritizes cash flow discipline, this trade-off is being penalized.

Not all AI exposure behaves the same — a distinction we break down further in our AI stocks analysis.

The AI subsectors showing resilience

Not all AI exposure is behaving the same way.

Relative strength is visible in:

- AI infrastructure and compute providers

Structural demand and pricing leverage remain intact. - Semiconductor companies with strategic positioning

These firms are difficult to replace and essential to the AI stack. - Vertical AI solutions with immediate ROI

Industrial automation, logistics optimization, energy systems, and defense applications. - Cash-generative businesses with AI as an enhancement

AI strengthens existing models rather than justifying them.

These segments are valued less on narrative and more on operational reality.

Index concentration and AI exposure risk

A critical but often overlooked factor behind recent volatility is concentration risk.

AI exposure has become increasingly concentrated within a small group of large technology companies. Within indices such as the NASDAQ, this creates amplification effects:

- price moves become more correlated

- sentiment shifts propagate faster

- corrections become sharper and more synchronized

As AI weight within major indices increases, small changes in expectations can drive outsized market reactions — in both directions.

Why index concentration matters

As AI exposure becomes increasingly concentrated in a small number of large technology stocks, index-level movements are amplified. This chart illustrates how technology has gained a dominant share of the S&P 500 over time, while low-profitability companies have steadily lost weight — increasing both upside potential and downside volatility during expectation shifts.

Implications for investors

The central takeaway is clear: AI is not a single investment category.

For investors, this environment favors:

- selectivity over broad exposure

- fundamentals over narratives

- understanding where AI creates cash flow — and where it consumes it

AI remains a long-term growth driver, but returns will not be evenly distributed. The era of indiscriminate AI optimism is fading.

For a broader framework on how AI fits into long-term portfolios, see our AI investing hub.

Implications for companies and AI strategy leaders

Beyond markets, the correction carries an important signal for businesses.

AI strategies driven primarily by optics or competitive fear are increasingly exposed. Sustainable implementations share common traits:

- clear cost-benefit frameworks

- measurable productivity gains

- phased deployment

- disciplined capital allocation

As financial markets mature, so too must corporate AI strategy. Execution now matters more than ambition.

Conclusion: not an AI crisis, but a reality check

The current pullback may feel uncomfortable, but it is fundamentally healthy.

Markets are shifting:

- from promises to proof

- from hype to execution

- from broad enthusiasm to selective conviction

AI remains a defining force in technology and economics. But its investment cycle is entering a more disciplined phase — one where fundamentals, not headlines, determine outcomes.

For those willing to look beyond short-term volatility, this is not the end of the AI story — but the beginning of a more mature one.

This correction does not change the structural trajectory of AI, which we track in our State of AI analysis.

Sources & Data References

- Piper Sandler — Equity strategy research on technology sector concentration and market leadership

- Nationwide Investment Research — S&P 500 sector weighting and profitability analysis

- S&P Dow Jones Indices — Historical S&P 500 sector composition data

- Federal Reserve Economic Data (FRED) — Interest rate and macroeconomic context

- Company earnings reports & investor presentations — Selected large-cap technology firms

- Arti-Trends Market Analysis — Editorial synthesis and interpretation of publicly available data

This analysis reflects market conditions at the time of publication. Market dynamics may change as earnings, interest rates, and AI adoption evolve.