Artificial intelligence has moved from experimental technology to strategic infrastructure in less than a decade. Capital is flowing into semiconductor manufacturers, hyperscale cloud providers, foundation model developers and AI-enabled application companies at scale. Yet believing in the long-term impact of AI is not the same as generating consistent investment returns from AI-related assets. The risks of investing in AI are distinct, multi-layered and often underestimated during periods of optimism.

For readers seeking a broader structural overview, our guide on What Is AI Investing? A Complete Guide to Stocks, ETFs & Crypto explains how AI exposure fits within diversified portfolios. This article focuses specifically on AI investing risks — the structural forces that shape downside scenarios as much as upside potential.

AI functions as a general-purpose technology, comparable in economic scope to electricity or the internet. That breadth creates powerful growth narratives but also amplifies systemic exposure. When capital concentrates around a transformative theme, equity markets can become increasingly dependent on a narrow group of dominant firms.

Recent assessments from the International Monetary Fund highlight rising concentration risk in global equity markets, particularly within technology-driven indices. AI has intensified this pattern. Major equity benchmarks are increasingly influenced by a limited number of companies tied directly to AI infrastructure, data centers and model deployment. When a small group of firms drives index performance, volatility in those firms reverberates more broadly through passive funds, pension allocations and global capital flows.

Concentration risk does not automatically imply fragility. However, it increases systemic sensitivity. Earnings disappointments, regulatory interventions or shifts in institutional positioning can produce outsized index-level effects when exposure is clustered.

Market Structure and Capital Flow Dynamics

Beyond company-level risk, AI investing is shaped by market structure. Passive capital has grown steadily over the past decade, and thematic ETFs focused on AI and technology have attracted substantial inflows. When new capital enters thematic funds, it is often allocated proportionally to existing holdings — typically reinforcing exposure to already dominant firms.

This creates a feedback mechanism. Strong performance attracts inflows. Inflows drive additional buying pressure. Elevated valuations reinforce performance narratives. Under stable conditions, this dynamic supports upward momentum. However, during narrative reversals, the same mechanism can amplify downside volatility as outflows force proportional selling across concentrated holdings.

Liquidity risk also becomes relevant in momentum-driven phases. When expectations shift — whether due to earnings surprises, regulatory developments or macroeconomic tightening — valuation compression can occur quickly. AI hype cycle investing is therefore not merely about sentiment; it is intertwined with structural capital allocation patterns that influence price behavior.

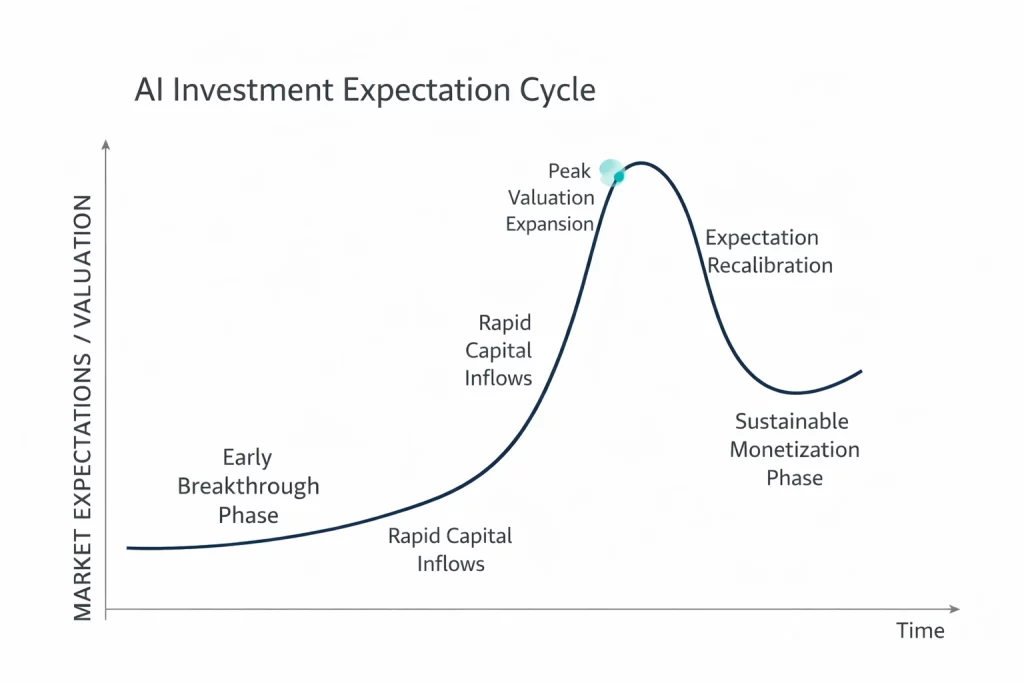

Hype Cycles and Narrative-Driven Valuation

This simplified investment expectation cycle illustrates how AI investing risks often emerge when valuation expansion accelerates faster than monetization.

One of the most visible AI investing risks is narrative acceleration. Technological breakthroughs generate headlines; headlines attract capital; capital inflows expand valuations; rising valuations reinforce belief. This cycle compresses the time between innovation and investor expectation.

Enterprise adoption data confirms rapid AI integration. Global surveys by McKinsey & Company show that organizations are embedding AI tools into workflows at increasing rates. However, monetization remains uneven. Adoption does not guarantee sustained margin expansion. When markets price long-term dominance before revenue models stabilize, valuation risk emerges.

AI valuation risk is therefore not about questioning technological progress. It concerns whether pricing reflects realistic earnings trajectories. During heightened enthusiasm, multiple expansion may outpace earnings growth. When expectations moderate, compression can occur even if technological progress continues.

Investors comparing long-term allocation with shorter-term positioning may find useful context in our analysis of AI Investing vs AI Trading, which explains how risk manifests differently across time horizons.

Regulatory and Geopolitical Risk

AI operates within evolving legal frameworks that vary by region. The European Commission’s AI Act introduces a risk-based classification system that imposes stricter compliance obligations on high-risk applications. Documentation, auditability and governance requirements increase operational complexity and cost.

Regulation redistributes opportunity rather than eliminating it. Larger firms may absorb compliance burdens more easily, potentially strengthening incumbency advantages. Smaller innovators may face margin pressure or slower deployment timelines. AI regulation risk therefore reshapes competitive dynamics across regions.

Geopolitical considerations add another dimension. Advanced AI systems depend on high-performance semiconductor manufacturing and energy-intensive infrastructure. Export control measures issued by the U.S. Department of Commerce restricting advanced chip transfers underscore the strategic importance of AI hardware. Semiconductor supply chains are geographically concentrated, exposing investors to policy shifts, trade tensions and capacity bottlenecks.

Capital Intensity and Infrastructure Exposure

AI infrastructure is capital-intensive. Data center expansion, GPU procurement, cooling systems and energy contracts require substantial upfront investment before incremental revenue materializes. This creates a structural lag between capital expenditure and monetization.

Energy exposure represents an additional variable. High-performance computing clusters consume significant electricity. Changes in energy pricing, grid constraints or sustainability regulation can influence cost structures. In periods of aggressive infrastructure build-out, return on invested capital may compress temporarily as firms scale capacity ahead of demand realization.

Infrastructure-heavy exposure amplifies earnings volatility. Companies tied to this layer may experience fluctuations driven more by investment cycles than by demand weakness. Investors examining this segment in detail can consult our analyses of AI stocks and thematic exposure through AI ETFs, both of which assess concentration, capex intensity and sector weighting dynamics.

Valuation Complexity and Optionality Risk

Many AI-driven firms operate with high research and development intensity and delayed profitability. Traditional valuation metrics may struggle to capture long-term optionality embedded in platform models.

Paying for potential network effects can be rational when competitive advantages are durable. However, rapid innovation cycles, open-source model development and commoditization pressures introduce execution risk. Open ecosystems can erode pricing power if differentiation is not sustained.

Optionality is valuable, but it is uncertain. When valuations reflect best-case scenarios across multiple business lines simultaneously, risk asymmetry increases. Small deviations from projected growth paths can have disproportionate valuation impact.

Disruption and Competitive Margin Pressure

AI creates new winners, but it also compresses margins across industries. Automation reduces production costs yet intensifies competition. Software-as-a-service providers, search-driven platforms and creative industries are adapting to generative systems that alter value chains.

The World Economic Forum’s Future of Jobs Report highlights both productivity gains and displacement pressures associated with AI adoption. From an investment perspective, disruption risk implies that even firms integrating AI capabilities may face transitional volatility if legacy revenue streams weaken or competitive intensity rises.

In decentralized ecosystems, AI-related tokens introduce additional layers of uncertainty, including regulatory ambiguity and network adoption variability. Our explainer on AI tokens and their utility models examines how token economics differ structurally from equity ownership models.

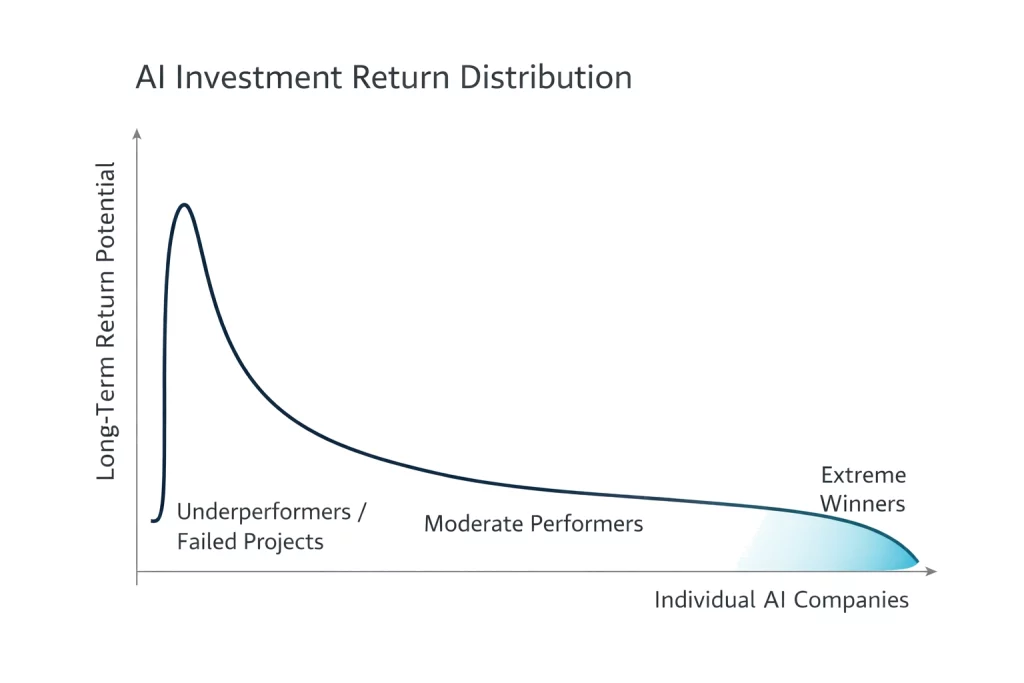

Return Dispersion and Winner Concentration

Transformative technology cycles historically produce highly uneven return distributions. A small number of firms capture outsized economic value, while many participants deliver modest or negative long-term returns.

Survivorship bias often distorts perception. After a cycle matures, attention focuses on the dominant winners. The broader field of unsuccessful or mediocre performers fades from collective memory. AI investing is likely to follow a similar pattern. The presence of extraordinary winners does not eliminate the probability of widespread underperformance among secondary players.

Return dispersion risk means that broad thematic exposure may not automatically capture the full upside narrative. Concentrated positions in dominant firms increase volatility; overly broad exposure may dilute performance if capital is allocated to structurally weaker participants.

Asset-Specific Risk Differences

Public AI equities are subject to liquidity cycles, institutional positioning shifts and earnings volatility. Passive inflows into thematic funds can amplify price movements in concentrated holdings.

Private AI startups face illiquidity, dependency on funding cycles and valuation markdown risk during tighter capital conditions. AI-related crypto assets introduce additional volatility linked to regulatory interpretation and network growth. Treating all AI exposure as homogeneous obscures these structural differences.

A Practical Risk Framework for Investors

A disciplined framework mitigates narrative volatility. Diversifying across infrastructure providers, model developers and application-layer firms reduces dependency on a single monetization pathway. Position sizing discipline prevents excessive concentration during hype phases. Valuation checks grounded in realistic revenue growth assumptions anchor expectations.

Monitoring regulatory developments across major jurisdictions remains essential, as compliance shifts can materially alter cost structures and competitive balance. Periodic thesis review ensures that investment decisions remain aligned with evolving fundamentals rather than legacy enthusiasm.

AI investing risks are structural, not episodic. Transformative technologies generate cycles of overenthusiasm followed by recalibration. Infrastructure tends to endure; valuation excess does not. Artificial intelligence is likely to remain embedded across industries for decades. Equity outcomes, however, will be uneven. Investors who approach AI exposure with disciplined risk assessment rather than narrative momentum are better positioned to navigate that dispersion.

Conclusion

Artificial intelligence is not a temporary market theme. It is becoming embedded in infrastructure, enterprise software, digital services and industrial systems. Its long-term economic relevance appears durable.

Financial returns, however, will not be evenly distributed.

AI investing risks arise from structural concentration, capital intensity, regulatory evolution and competitive disruption. Valuation cycles may overshoot. Capital flows may amplify momentum in both directions. Infrastructure build-outs may compress short-term returns before durable profitability emerges.

The central question is therefore not whether AI will matter, but how value will be captured — and at what price investors gain exposure.

History suggests that transformative technologies create extraordinary winners alongside widespread underperformance. Disciplined capital allocation, diversification across layers and valuation realism matter more than narrative conviction.

For a broader strategic overview of AI exposure across asset classes, return to the AI Investment Hub, where stocks, ETFs and crypto segments are mapped within a unified framework.

AI will continue to evolve. Market expectations will evolve with it. The investors best positioned for long-term outcomes will be those who understand both.

Sources & References

- International Monetary Fund — Global Financial Stability Report

- McKinsey & Company — Global AI Survey

- European Commission — AI Act

- U.S. Department of Commerce — Export control measures on advanced AI-related technologies

- World Economic Forum — Future of Jobs Report